where: - \(w\) is the weight in

asset 1 (so \(1-w\) is the weight in

asset 2) - \(\mu_1, \mu_2\) are the

expected returns - \(\sigma_1,

\sigma_2\) are the standard deviations - \(\rho_{12}\) is the correlation between the

two assets

The efficient frontier consists of the portfolios on

the upper branch of this curve—those with the highest expected return

for a given level of risk.

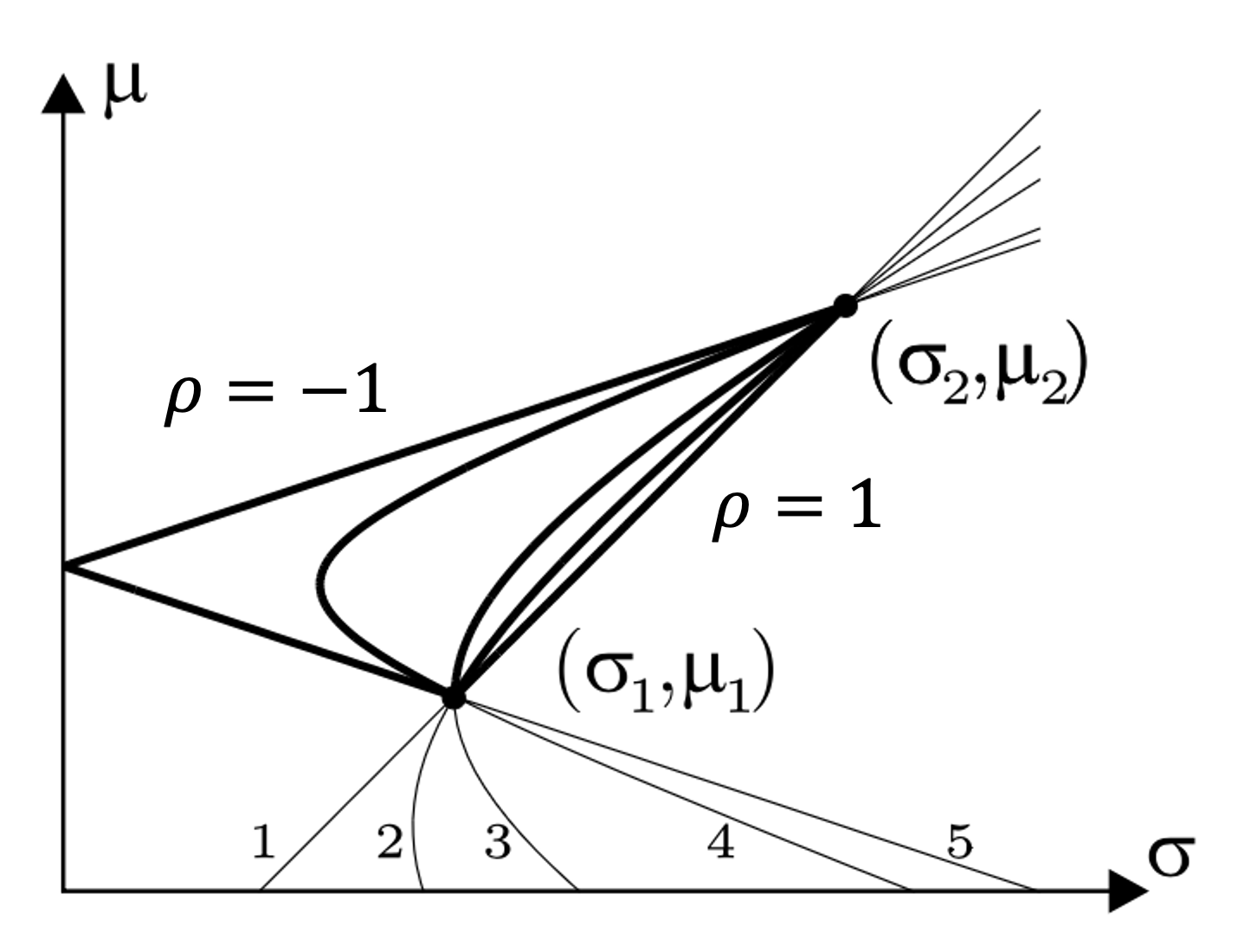

Two-asset Efficient

Frontier

Each point corresponds to a value of \(w\) (the weight in asset 1).

The upper part of the curve is

efficient—these portfolios offer the best return for a

given risk.

The lower part of the curve is

dominated—there are always better choices

available.

The endpoints correspond to holding 100% of one

asset (either asset 1 or asset 2).

Diversification (choosing \(0 < w < 1\)) improves the risk-return

trade-off compared to holding a single asset.

Conditions for the Efficient

Set

The conditions for the efficient set (relative to asset 1) are:

If \(\frac{\sigma_1}{\sigma_2} <

\rho_{12} \leq 1\), then there exists a portfolio with

short selling such that \(\sigma_V

< \sigma_1\), but for each portfolio without short

selling\(\sigma_V \geq

\sigma_1\) (lines 1 and 2).

If \(\rho_{12} =

\frac{\sigma_1}{\sigma_2}\), then \(\sigma_V \geq \sigma_1\) for each portfolio

(line 3).

If \(-1 \leq \rho_{12} <

\frac{\sigma_1}{\sigma_2}\), then there exists a portfolio

without short selling such that \(\sigma_V < \sigma_1\) (lines 4 and

5).

These conditions describe when diversification can reduce risk below

that of the less risky asset, depending on the correlation and the

possibility of short selling.

Minimum Variance Portfolio

(MVP)

The Minimum Variance Portfolio (MVP) is the

portfolio with the lowest possible risk (variance) for given assets.

This gives the unique portfolio with the lowest possible variance for

two assets.

How?Minimize\(\sigma_V^2\) subject to \(w_1 + w_2 = 1\).

Derivation Using the

Lagrangian

Suppose we have two assets with weights \(w_1\) and \(w_2 =

1 - w_1\). The portfolio variance is: \[

\sigma_V^2 = w_1^2 \sigma_1^2 + (1-w_1)^2 \sigma_2^2 +

2w_1(1-w_1)\rho_{12}\sigma_1\sigma_2

\]

We want to minimize\(\sigma_V^2\) subject to \(w_1 + w_2 = 1\).

Lagrangian Setup

Let \(\lambda\) be the Lagrange

multiplier: \[

\mathcal{L}(w_1, w_2, \lambda) = \sigma_V^2 - \lambda(w_1 + w_2 - 1)

\]

But since \(w_2 = 1 - w_1\), we can

write everything in terms of \(w_1\):

\[

\mathcal{L}(w_1, \lambda) = w_1^2 \sigma_1^2 + (1-w_1)^2 \sigma_2^2 +

2w_1(1-w_1)\rho_{12}\sigma_1\sigma_2 - \lambda(w_1 + (1-w_1) - 1)

\]

The constraint simplifies to \(w_1 + w_2 -

1 = 0\), which is always satisfied.

Take the Derivative

Set the derivative with respect to \(w_1\) to zero: \[

\frac{\partial \mathcal{L}}{\partial w_1} = 2w_1\sigma_1^2 -

2(1-w_1)\sigma_2^2 + 2(1-2w_1)\rho_{12}\sigma_1\sigma_2 = 0

\]

Expand and solve for \(w_1\): \[

2w_1\sigma_1^2 - 2\sigma_2^2 + 2w_1\sigma_2^2 +

2\rho_{12}\sigma_1\sigma_2 - 4w_1\rho_{12}\sigma_1\sigma_2 = 0

\]

For \(\rho_{12} < 1\), this

condition is always satisfied unless the assets are perfectly positively

correlated and have identical volatilities. Thus, the solution above

gives the minimum variance.

Derivation: Efficient Set

Conditions

To determine when diversification reduces portfolio risk below that

of the less risky asset, analyze the portfolio variance:

By design, \(\sigma_1 <

\sigma_2\). This implies \(\frac{\sigma_1}{\sigma_2} <

\frac{\sigma_2}{\sigma_1}\). So, the prevailing condition is:

\[

\rho_{12} < \frac{\sigma_1}{\sigma_2}

\]

Summary of Conditions

If \(\rho_{12} <

\frac{\sigma_1}{\sigma_2}\): There exists a portfolio

(without short selling) with risk less than \(\sigma_1\).

If \(\rho_{12} =

\frac{\sigma_1}{\sigma_2}\): The minimum risk equals

\(\sigma_1\); no further reduction is

possible.

If \(\rho_{12} >

\frac{\sigma_1}{\sigma_2}\): Diversification cannot

reduce risk below \(\sigma_1\) without

short selling.

These conditions define when the efficient set includes portfolios

with risk lower than the least risky asset, depending on correlation and

asset volatilities.

Derivation:

Efficient Frontier Equation for Two Assets

Consider two risky assets with expected returns \(\mu_1\), \(\mu_2\), standard deviations \(\sigma_1\), \(\sigma_2\), and correlation \(\rho_{12}\). Let \(w\) be the weight in asset 1, so \(1-w\) is the weight in asset 2.

Portfolio Expected Return

The expected return of the portfolio is: \[

\mu(w) = w \mu_1 + (1-w) \mu_2

\]

Portfolio Variance

The variance of the portfolio is: \[

\sigma^2(w) = w^2 \sigma_1^2 + (1-w)^2 \sigma_2^2 +

2w(1-w)\rho_{12}\sigma_1\sigma_2

\]

Efficient Frontier Equation

To express the efficient frontier, eliminate \(w\) in favor of \(\mu\):

Solve for \(w\): \[

\mu(w) = w \mu_1 + (1-w) \mu_2 \implies w = \frac{\mu(w) - \mu_2}{\mu_1

- \mu_2}

\]